5G is the core engine that leads the innovation and development in the information field.

Text/Sina Financial Opinion Leaders Column research institute

5G may bring new kinetic energy to the next wave of economic growth and have a positive impact on various industries around the world. The vertical application of the three technical scenarios of 5G in the fields of cloud (cloud computing), network (communication network) and terminal (intelligent terminal) will accelerate the digital transformation of traditional industries and bring certain industrial investment opportunities.

■ 5G is the core engine leading the innovation and development in the information field. Historically, countries with the first-Mover advantage in mobile communication have gained huge economic benefits. 5G may bring new kinetic energy to the next wave of economic growth and have a positive impact on various industries around the world. The vertical application of the three technical scenarios of 5G in the fields of cloud (cloud computing), network (communication network) and terminal (intelligent terminal) will accelerate the digital transformation of traditional industries and bring certain industrial investment opportunities.

■ 5G network construction drives capital expenditure into a new rising cycle. The construction of 5G network has gone through three stages: standard setting, spectrum auction and investment construction. Choosing the construction path of different frequency bands may determine the success or failure of 5G network investment. Global operators actively deploy 5G network construction, and China, South Korea and Japan lead the global 5G commercialization. With the landing of China’s 5G commercial license, the scale construction and commercialization of 5G have begun. It is estimated that China’s 5G network investment will exceed one trillion, and the investment opportunities of China’s communication equipment enterprises and their supply chains are significant.

■ Diversification of 5G terminals brings medium and long-term investment opportunities. From the perspective of industrial development path, 5G terminals will gradually evolve from the consumer terminals of the Internet of People to the Internet of Things terminals of the Internet of Everything, and the terminal types are diversified. The maturity of the supply chain has driven the rapid development of the consumer terminal market. In the next three years, 5G mobile phones are expected to usher in explosive growth, and the scale of the 5G terminal market will far exceed the scale of investment in 5G networks. The terminal market of Internet of Things will maintain a long-term high growth rate, and the terminal markets of smart home, car networking and industrial Internet of Things have medium and long-term investment opportunities.

■ 5G industry cloud has long-term development prospects in the vertical field. From the perspective of application scenarios, 5G promotes the convergence of cloud network services, and gradually evolves from a cloud platform that provides virtualized basic resources to an industry cloud in a typical vertical field. 5G not only continues to drive the rapid growth of data center infrastructure, but also further integrates with education, security, entertainment, finance, energy, industry and other fields to create new kinetic energy for economic development.

In the past 40 years, a new generation of revolutionary technology has emerged in mobile communication every decade. The new technology has continuously promoted the rapid development of the information technology industry and promoted the prosperity and development of all fields of the global economy and society.

The fifth generation mobile communication technology (5G) has arrived. As the infrastructure of the new generation information industry, 5G network has three characteristics: ultra-high speed, ultra-large connection and ultra-low delay. The construction of 5G network will accelerate the development of upstream and downstream industrial chains such as communication, electronics, computers, semiconductors, Internet, artificial intelligence and big data, and drive the digital transformation of vertical industries such as industry, automobile, energy, medical care, finance and public utilities. The Internet of Everything changes the mode of production and organization of human beings, and intelligent manufacturing promotes the optimization of industrial structure and efficiency, thus promoting the transformation and upgrading of traditional industries and promoting the sustained and rapid development of the global economy and society.

This report starts with the impact of communication technology changes on global economic and social development, and analyzes the industrial maturity and investment opportunities of 5G in various fields from three aspects: cloud (cloud platform), network (communication network) and terminal.

1.5G is the core engine leading the innovation and development in the information field.

1.1 Countries with first-Mover advantage in mobile communication have gained huge economic benefits.

Countries with first-Mover advantage for each generation of mobile communication have a major share of the global market in their domestic industrial chains. Modern mobile communication originated from the concept of cellular network in 1970s. With the progress of science and technology in 1980s, the global mobile communication network developed rapidly. AMPS system, represented by Motorola, USA, led the global communication market in the 1G era by virtue of its technological advantages.

In the 2G era, Europe learned many lessons from the 1G era and took the lead in promoting the construction of 2G networks by adopting a unified GSM standard. European communication enterprises such as Ericsson, Nokia, Alcatel and Siemens rose up, leading the global industrial chain and bringing huge economic benefits to Europe. With the backwardness of the United States in the 2G communication market, Motorola, Lucent and other companies in the United States have stepped down from the peak of history.

In the 3G era, Europe thought the business prospect was unclear, hesitated on 3G deployment, and did not form an ecosystem of mobile phone industry. Japan seized this opportunity and made a profit in a brand-new way. In 1999, NTT DOCOMO, a Japanese operator, launched the i-mode mobile phone ecosystem, which provided internet services such as surfing, social networking and music. I-mode was launched eight years earlier than Apple’s iOS ecosystem, which brought huge commercial benefits to the Japanese industrial chain represented by NTT and NEC.

In the 4G era, the United States corrected its previous mistakes. The Federal Communications Commission actively carried out spectrum auctions and allowed operators to use frequency bands more flexibly to build networks. The birth and rise of Apple’s iPhone and iOS, as well as the global promotion of Android, laid the foundation for the global leadership of the 4G era in the United States. However, Japan’s i-mode system has not been promoted globally. From the early days of 4G, Japan kept pace with the United States, and the United States completely occupied the global control of 4G in the later period. What followed was that NEC, Panasonic, Toshiba and Fujitsu in the i-mode ecosystem gradually withdrew from the smart phone market, and international brands such as Apple, Samsung, Huawei and OPPO rose in an all-round way by relying on the iOS and Android eco-chains.

Figure 1: Development of Mobile Communication

Source: China Merchants Bank Research Institute

The Influence of Leading in the 4G Era on American Economy

America’s leading position in 4G has made great contributions to the American economy. In the 4G era, the contribution of the mobile communication industry to the GDP of the United States increased from the original forecast of $350.3 billion in 2016 to $445 billion. From 2011 to 2014, the number of jobs related to mobile communication increased by 84%. In 2016, the international revenue brought by 4G to American companies reached $125.5 billion. Among them, the income from equipment manufacturing and sales is 64.9 billion US dollars, the international income from application stores is 25 billion US dollars, and the international income from equipment components is 35.6 billion US dollars. The content revenue of the app store has also increased rapidly, from $8.2 billion in 2011 to $54.1 billion in 2016.

Figure 2: The influence of 2:4G on the GDP of American mobile communication.

Source: Recon Analytics, China Merchants Bank Research Institute

Figure 3: Impact of 3:4G on App Store Revenue

Source: Recon Analytics, China Merchants Bank Research Institute

Looking back on the development process from 1G to 4G, every country with leading mobile communication technology leads the global mobile communication market, and its domestic mobile communication enterprises occupy a major share in the world and have gained huge economic benefits. When these countries lost their leadership in mobile communication technology, their domestic communication enterprises suffered a blow. The development of a new generation of communication technology is expected to create new kinetic energy for the innovation-driven economy.

1.2 5G may bring new kinetic energy to the next wave of economic growth.

5G has a positive impact on the global economy

5G will have a positive impact on all industrial sectors. According to IHS Markit’s estimation, by 2035, the global output generated by 5G will reach $12.3 trillion. Among them, the manufacturing industry achieved an output of about 3.4 trillion US dollars (accounting for 28% of the total output), and the information and communication industry achieved an output of about 1.4 trillion US dollars, followed by wholesale and retail, public services, construction, finance and insurance, transportation and storage, professional services, hotels, agriculture, forestry and fisheries, real estate, education, public utilities, mining, health and social work, art and entertainment.

5G may make a great contribution to China’s economic output. According to the model calculation of China ICT Institute, in terms of output scale, the direct output and indirect output of China’s economy driven by 5G will reach 6.3 trillion yuan and 10.6 trillion yuan respectively in 2030. In terms of direct output, the compound annual growth rate in the past ten years is 29%. In terms of indirect output, the compound annual growth rate is 24%. From the contribution to economic added value, it is estimated that the GDP directly created and indirectly pulled by 5G will be 3 trillion and 3.6 trillion respectively in 2030. The compound annual growth rate of GDP directly created by 5G is about 41%; The compound annual growth rate of GDP indirectly driven by 5G will reach 24%.

5G has a conductive effect on social and economic development. 5G can stimulate various industrial sectors to increase digital investment, accelerate the digital transformation of traditional industries, promote business application innovation, expand the international market space of information products, and enhance China’s comprehensive advantages.

Figure 4: Global 5G Support Industry Output Forecast in 2035

Source: IHS Markit, China Merchants Bank Research Institute.

Figure 5: The Impact of 5:5G on China’s Economy

Source: China ICT Institute, China Merchants Bank Research Institute.

The three major scenarios of 5G continue to drive economic transformation and upgrading

From the development path of the global information industry, the Internet of Everything has to go through three stages: people, people and machines, and machines and machines. Judging from the development sequence of the three major technical scenarios of 5G, the first stage (2019-2021) takes people first, and the large bandwidth (eMBB) application scenario is the main one; In the second stage (2021-2023), human-computer interaction and mMTC Internet of Things applications rose in an all-round way; In the third stage (2023-long-term), all things are connected, and industrial control applications with low latency (uRLLC) are gradually maturing.

Figure 6: Three Application Scenarios of 6:5G

Source: China Merchants Bank Research Institute

The characteristics of 5G technology will catalyze three kinds of scenarios and accelerate the digital transformation of traditional industries. Compared with the single human-to-human communication scenario of 4G, 5G will support three scenarios: eMBB (Enhanced Mobile Broadband), mMTC (Large-scale Machine Communication) and uRLLC (High Reliability and Low Delay Communication). The main vertical application fields include industry, automobile, energy, medical care, finance and public utilities. The intersection of the three technical scenarios and vertical industries is expected to form a variety of application ecology between people and things, things and things, and promote the digital transformation and upgrading of traditional industries.

EMBB high-traffic mobile broadband scenario, to improve the network capacity to meet the needs of large bandwidth, the network peak rate can reach 1-10 G. The construction of 5G network in 2019-2021 is mainly to provide network services for eMBB scenarios. The 5G base station, transmission network and core network on the network side have great investment opportunities. Based on eMBB scenario, 5G terminals are diversified, and the categories of mobile phones, tablets, 4K/8K TVs, AR/VR terminals, security terminals and vehicle terminals are becoming more and more abundant. The application scenarios are more subdivided and diversified, and cloud AR/VR, cloud games, cloud video, cloud education, etc. provide life and entertainment services in large bandwidth scenarios.

MMTC large-scale Internet of Things scenario, which effectively supports massive Internet of Things devices access, and the connection density can reach 1 million/km2. In 2021-2023, the 5G network will be upgraded by NB-IoT, and the core network will be completely SA-independent. 5G terminals have exploded in many fields such as smart wear, smart home, intelligent transportation, and intelligent logistics. Cloud applications meet the needs of terminals, and there are platforms for Internet of Things segments such as cloud logistics, cloud transportation and cloud industry, which cooperate with the unified networking, management and operation of things.

The high-reliability and low-delay scenario of uRLLC belongs to the control application scenario, and the transmission delay can reach millisecond, which will be an important growth field of 5G. 5G network construction after 2023 will pay more attention to network slicing and edge computing capabilities, and provide ultra-low delay network capabilities; The 5G terminals in the uRLLC scene are mainly self-driving vehicles and industries.Intelligent equipment such as automatic control equipment and service robots; Cloud applications meet the needs of smart devices and provide control applications that meet the stringent requirements of the industrial Internet, such as cloud autopilot, cloud industrial control and cloud services.

1.3 Investment Path of 5G Industry

From the development path of global information industry, 5G has certain industrial investment opportunities in cloud (cloud platform), network (communication network) and terminal (terminal) industrial chains.

Cloud platform develops from basic service to industry cloud service. In the past ten years, cloud computing technology has developed rapidly, and it has become a trend for enterprises to go to the cloud. The three basic service modes of cloud computing (IaaS, PaaS and SaaS) have been fully matured, and they are constantly expanding to the deeper industrial application field of XaaS. Focusing on the digital upgrade of vertical industry applications, 5G will promote the traditional vertical industries such as education, medical care, energy and industry to generate new cloud demand, and build a new intelligent cloud architecture with cloud network integration, edge cloud collaboration and comprehensive cloud services.

Figure 7: Industrial Topology of 7:5G Cloud Network

Source: China Merchants Bank Research Institute

The network layer advances from serving consumer terminals to the intelligent scheduling architecture of the Internet of Everything. In order to support the 5G characteristics of large bandwidth, large connection and low delay, key technologies and networking schemes such as new antenna air interface technology, large-scale antenna array, wireless network CU/DU (centralized/distributed) architecture, network slicing, edge computing and SDN (software-defined network) are adopted to create a new ecology for traditional vertical industries and open up huge value growth space for the industry.

The terminal layer is constantly spreading from consumer terminals to Internet of Things terminals in traditional industries. 5G terminals will be integrated with more and more industries, thus realizing more functions and services. New products such as wearable devices, smart homes, vehicle terminals, educational robots and service robots are constantly emerging, showing a diversified development trend in the future, accompanied by more and more Internet of Things applications, and the Internet of Everything will then push the terminal market into a new development height.

2.5G network construction drives capital expenditure into a new rising cycle.

The construction of 5G network has to go through three stages: standard setting, spectrum auction and investment construction. The progress of each stage directly affects the final completion and commercial operation of the 5G network, and choosing the construction path of different frequency bands may determine the success or failure of the 5G network investment.

2.1 5G standard spectrum landing promotes commercial acceleration

The 5G standard has gradually landed and commercial applications have been launched one after another.

The greater the contribution to the technology of the 5G standard, the more patents of 5G SEP, and the more dividends of the 5G industry will be shared in the future.

R15, the standard of large bandwidth eMMB scene, landed first. Judging from the freezing sequence of 5G standards, R15 has been frozen in the first stage, and applications that need large bandwidth, such as 4K live broadcast, security monitoring, VR video and so on, will take the lead in popularization and application, and related chips, network equipment and terminal industrial chain are all mature and have the conditions for large-scale networking construction.

Figure 8: 5 G standard promotion and industrial chain progress

Source: GSA, China Merchants Bank Research Institute

The standards for Internet of Things (mMTC) and low latency (uRLLC) scenarios will be discussed and improved in the second phase of R16 and R17 standards. At present, the Internet of Things is dominated by NB-IoT, LoRa and eMTC technologies, and it is expected that NB-IoT will continue to be adopted as the standard of 5G Internet of Things in R16 version to ensure the continuity of network investment and user services from 4G era to 5G era. The R16 standard will be frozen until 2020. The R17 standard will be established at the end of 2019, and the R17 standard will be frozen until 2022, and the maturity of related vertical industries is expected to be after 2023.

Chinese enterprises have the advantages of global 5G patents and standards. Judging from the global number of patent applications for 5G SEP (standard necessity) and the global contribution of 5G standard technology, China has become the first group of 5G in the world. SEP patent refers to the patent that is included in international standards and must be used in the implementation of standards, that is to say, when standardization organizations formulate certain standards, they must be involved. With a large number of 5G SEP patents, it has a strong industry leading edge. Judging from the contribution of 5SEP patents and 5G standard technologies, Huawei and ZTE have become the first group, and OPPO has entered the forefront of the world through years of advanced layout and active R&D investment. The advantages of 5G patents and standards lay a solid foundation for future industry competition.

Figure 9: Global patent applications for 5G SEP (July 2019)

Source: IPlytics, China Merchants Bank Research Institute.

Figure 10: Global 5G standard technology contribution (July 2019)

Source: IPlytics, China Merchants Bank Research Institute.

With the acceleration of global spectrum auction, network investment is imminent.

In order to speed up the construction of 5G, countries around the world have accelerated the auction of 5G spectrum. The coverage of 5G network needs the spectrum of low frequency band (below 2GHz), middle frequency band (2GHz to 6GHz, also called Sub-6) and high frequency band (above 6GHz, also called millimeter wave) to realize the complete vision of IMT-2020 mobile broadband for the mass market. According to GSA statistics, as of August 2019, 71 countries/regions around the world are considering or allocating 5G spectrum, 34 countries/regions have completed the auction of at least one frequency band suitable for 5G, and 40 countries have announced plans to continue the auction of 5G spectrum between 2019 and 2021.

The intermediate frequency band is the best deployment frequency band for 5G, which has the characteristics of wide coverage and high capacity. The intermediate frequency band 3.3-4.2GHz is the most widely used 5G frequency band in the world, and it has been regarded as the main frequency band for 5G network construction by most countries. Korea, China and Japan took the lead in mid-band spectrum planning and allocation and 5G construction. Among them, South Korea allocated 3.42-3.7GHz, China allocated 2.515-2.675GHz, 3.5-3.7GHz and 4.8-4.9GHz, and Japan allocated 3.6-4.1GHz.

High-frequency band has a wider continuous spectrum, which can provide greater network speed. However, taking high-frequency band as the main construction frequency band of 5G has a huge investment scale and great investment risk. The United States has always wanted to be the leader of 5G, but because the mid-band spectrum has been occupied, the Federal Communications Commission auctioned the high-band spectrum of 37.6 GHz–38.6 GHz, 38.6 GHz–40 GHz and 47.2 GHz–48.2 GHz for 5G construction. The high-frequency band has the problems of short coverage distance of base stations and a large number of base stations for continuous coverage, while the frequency clearing and re-auction in the middle-frequency band in the United States will be in 2020 at the earliest, which may greatly delay the deployment process of its 5G. American operators Verizon and AT&T use high-band millimeter waves to launch 5G services, but their 5G network coverage is very limited. Therefore, American 5G is still in its infancy in terms of network coverage, performance and industrial application.

Figure 11: Global 5G spectrum distribution (August 2019)

Source: GSA, China Merchants Bank Research Institute

2.2 5G network investment ushered in a new round of rising cycle.

Countries have successively started to invest in 5G networks.

Global operators actively deploy 5G networks. From the second half of 2018 to the first half of 2019, countries have successively started 5G commercialization or related processes. As of August 2019, 296 operators in 100 countries are launching or conducting related 5G trials, of which 56 operators in 32 countries have announced the deployment of 5G networks, and 39 operators have announced the launch of 5G services.

Figure 12: Global 5G Commercial Time (August 2019)

Source: GSA, China Merchants Bank Research Institute

Figure 13: Global 5G Network Investment Progress (August 2019)

Source: GSA, China Merchants Bank Research Institute

The construction of 5G network is still in the early stage, and the number of commercial networks is still small. The proportion of global operators who have deployed 5G networks is only 19%. Most operators are still in the process of evaluation, testing, license application and network planning. The scale of deployed 5G networks is also small, and the construction of global operators’ 5G networks is still moving forward.

China, South Korea and Japan lead the promotion of global 5G commercialization. The development process of 5G is expected to go through the process from policy-driven to business-driven, and it is still in the policy-driven stage. China, Japan, South Korea and Europe are the first countries to commercialize 5G.

Table 1: Progress of 5G Commercialization in Major Countries in the World

Source: China Merchants Bank Research Institute

China’s 5G network investment may exceed one trillion

5G issued a commercial license and the scale construction kicked off. On June 6, 2019, the Ministry of Industry and Information Technology、、5G commercial license issued by China Radio and Television. China Mobile, China Telecom and China Unicom are expected to spend 169.9 billion, 78 billion and 58 billion respectively in 2019. The total capital expenditure of the three major operators is 300 billion yuan, and the 5G part is about 33 billion yuan. Yang Jie, chairman of China Mobile, said that 5G construction will reach its peak in 2020-2022.

Figure 14: Five-G Networking Construction Strategies of Three Major Operators

Source: Operators, China Merchants Bank Research Institute.

The density of 5G base stations is expected to increase significantly. According to the propagation characteristics of electromagnetic waves, the frequency of electromagnetic waves is inversely proportional to the transmission distance. The higher the frequency of electromagnetic waves, the shorter the coverage distance of base stations. The main frequency band adopted by 2G is 900MHz, and the coverage radius is about 5-10 kilometers. 3G adopts 1.9-2.1GHz, with a coverage radius of about 2-5 kilometers; The main frequency bands adopted by 4G are 1.8-1.9GHz and 2.3-2.6GHz, and the coverage radius is about 1-3 kilometers. If 5G is used in the intermediate frequency bands of 2.6GHz, 3.4-3.6GHz and 4.8-4.9GHz, the coverage radius is about 300-500m. This means that the operating frequency band of 5G is higher, and the coverage of 5G base stations is smaller than that of 4G base stations. It is estimated that the number of 5G base stations will increase by 30%.

Figure 15: Relationship between Frequency Band and Base Station Coverage Distance

Source: China Merchants Bank Research Institute

Figure 16: 5 G base station coverage scenario

Source: China Merchants Bank Research Institute

Hong Jizhan is given priority to, supplemented by small base stations. There are three main scenarios for 5G network planning: dense urban areas, general urban areas and suburbs. The dense urban areas are mainly covered by high-capacity Hong Jizhan, the commercial office buildings are covered by medium and low-capacity room sub-systems, and the hot areas such as exhibitions and transportation hubs are covered by small base stations to realize high-quality and low-cost network construction. In general, the urban areas are mainly covered by Hong Jizhan with medium capacity, and the commercial office buildings are covered by low-capacity room sub-systems. Suburbs adopt low-capacity local key coverage in Hong Jizhan.

Telecom Unicom’s joint construction and sharing can be mutually beneficial and win-win. Under the condition of different 5G frequency bands and covering the same area, the number of 5G base stations to be built is also different. According to the ITU-3D NLOS road loss model test, the road loss at 3.5GHz is larger than that at 2.6GHz, and the penetration loss is higher. In the case of the same base station transmission power, the 3.5GHz band wants to cover the same area as the 2.6GHz band. Theoretically, the number of base stations of China Telecom and China Unicom is 38% higher than that of China Mobile. Therefore, the cooperation between China Telecom and China Unicom in the construction of 5G base stations can save money, give play to the sharing advantages and enhance the investment effect.

The investment scale of 5G is more than 50% higher than that of 4G. By the end of 2016, 3.15 million base stations had been built in the main investment period of 4G (2013-2016), including 1.51 million in China Mobile, 900,000 in China Telecom and 740,000 in China Unicom. Considering that the density of 5G base stations is significantly higher than that of 4G, according to the scale of 4G network investment, it is estimated that the three major operators will build 4 million 5G base stations in 2019-2022, and the number of 5G base stations will increase by about 27% compared with the number of 4G base stations in the same period in history. Among them, China Mobile has 2 million stations, and China Telecom and China Unicom have jointly built 2 million stations. The 5G base station adopts large-scale antenna technology, and the unit price of the base station is obviously improved; The 5G transmission network supports network slicing, and all transmission networks need to be newly built. The total investment of China’s three major operators in 4G reached 745 billion, according toAccording to the calculation of securities, China’s 5G network investment will be as high as 1.1 trillion yuan. Similar to the investment structure of 4G network, the largest capital expenditure is base station, followed by transmission network, core network and other operation support systems.

Table 2: Estimation of China’s Operators’ 5G Network Investment

Source: China Securities, China Merchants Bank Research Institute.

The investment rhythm of China’s 5G network

The capital expenditure of communication industry is cyclical. In the 3G and 4G era of operators, capital expenditure presents periodic changes, from small-scale construction one year before the issuance of licenses to large-scale construction three years after the issuance of licenses. The main construction period is four years. 3G license was issued on January 7th, 2009, and operators started to build 3G networks ahead of schedule in 2008. In 2008, operators’ capital expenditure showed signs of recovery, and 2009-2011 was the main investment period of 3G networks. The 4G license was issued on December 4, 2013, and operators began to build 4G networks in 2013. 2014-2016 is the main investment period of 4G networks. The 5G license was issued on June 6, 2019, and 2020-2022 will be the main investment period of 5G networks.

Two years after the issuance of the communication license, the capital expenditure peaked, and in the third year, the capital expenditure declined. The capital expenditure peaked in 2009-2010 after the issuance of 3G licenses, and in 2014-2015 after the issuance of 4G licenses. With the maturity of each generation of communication industry chain, following anti-Moore’s law, the cost and price of equipment in the third year of investment period decreased synchronously, which led to the reduction of capital expenditure of operators. From 2014 to 2016, the annual construction of 4G base stations of the three major operators reached 1.02 million stations, 1.07 million stations and 1.12 million stations respectively. Due to the price reduction of equipment, the capital expenditure in 2016 was lower than that in 2014 and 2015. 2019 is the first year of 5G investment and construction. It is estimated that 2020-2021 will be the peak period of 5G capital expenditure, and 5G capital expenditure will fall back in 2022.

Figure 17: Scale of Capital Expenditure of Three Major Operators

Source: Wind, China Merchants Bank Research Institute

Figure 18: Proportion of Capital Expenditure Structure of China Mobile

Source: Wind, China Merchants Bank Research Institute

The base station investment remained stable, and the transmission investment was concentrated in the early stage. From the path of network construction, the transmission network is built first, and the base station construction can be carried out on a large scale. From the perspective of China Mobile’s 4G investment process, transmission construction started early in 2013 before licensing, and the scale was gradually reduced in the later period; The scale of base station construction was small before licensing, and the base station investment was steadily advanced in 2014-2016 after licensing. It is estimated that the base station investment will be distributed smoothly in 2020-2022, the transmission investment will be concentrated in 2020-2021, and the stocking of the upstream supply chain will be about 3-6 months ahead of the capital expenditure of network equipment.

China’s communication equipment enterprises and supply chain investment opportunities are significant.

Huawei ZTE has a leading position in the global communication equipment market. According to the global communication equipment market report released by Dell‘Oro, the seven major equipment manufacturers in the world are Huawei, Nokia, Ericsson, Cisco, ZTE, Ciena and Samsung, which together account for about 80% of the global equipment vendors’ market share. Relying on the leading edge of standards and patents, Huawei’s market share in communication equipment continues to rise, and its global market share in 2019H1 reached 29%.After being punished by the United States in 2018, the global market share briefly fell to 7.7%, and in 2019H1, the market share was close to the historical high of 9.9%.

The upstream supply chain of Huawei ZTE has great investment opportunities. As of October 2019, from the published 5G commercial contracts, Huawei has more than 60 5G commercial contracts, more than 150,000 delivery base stations and more than 400,000 AAU modules. ZTE has more than 25 commercial contracts and more than 50,000 delivery base stations. The upstream supply chain enterprises with Huawei and ZTE as the core have shown signs of good overall performance and will have greater investment opportunities in the next 2-3 years.

3.5G terminal diversification brings medium and long-term investment opportunities.

From the development path of the 5G industry, 5G terminals will gradually evolve from consumer terminals dominated by the Internet of People to Internet of Things terminals dominated by the Internet of Everything. The terminal types are diversified, from mobile phones, AR/VR, smart wear and smart homes to car networking, commercial robots and industrial robots. 5G terminals have medium and long-term investment opportunities.

3.1 5G mobile phone market welcomes high growth opportunities.

The maturity of supply chain drives the rapid development of global 5G terminal market.

Global 5G mobile phones are experiencing explosive growth opportunities. From the global history of 4G development, the deployment of 4G networks has brought huge growth opportunities to the 4G smartphone market. The United States, Japan and South Korea started the construction of 4G networks in 2011, and China in Europe started the construction of 4G networks in 2013. The global construction of 4G networks has brought double-digit growth in the smartphone market for six consecutive years since 2010, and the scale of the 4G smartphone market has reached one trillion yuan. 5G network investment will help the global 5G mobile phone market usher in explosive growth opportunities. According to Strategy Analytics, by 2025, the global shipment of 5G mobile phones will exceed 1.5 billion. From 2019 to 2024, the shipments of 5G mobile phones will reach 2 million, 11 million, 77 million, 183 million, 416 million and 855 million respectively. IDC predicts that by 2020, 5G smartphone shipments will account for 8.9% of the total shipments, reaching 123.5 million units; By 2023, this proportion is expected to increase to 28.1%.

The global 5G terminal products are diversified. Through the joint efforts of the industry, the 5G mobile phone industry chain has matured. In 2019, major suppliers such as Qualcomm, Huawei, Samsung, MediaTek and Ziguang Zhanrui all launched 5G baseband chips. The maturity of the supply chain has promoted the rapid development of global 5G terminal products. China Mobile predicts that in 2020, more than 10 brands will launch 5G mobile phones, with more than 100 types of 5G mobile phones and terminals. According to GSA statistics, as of November 2019, there were more than 183 5G terminals in the world, involving 15 categories. Among them, there are 54 models of 5G mobile phones, 59 models of CPE (network terminal equipment), 34 models of 5G modules, 11 models of 5G hot products and 7 models of 5G routers. The diversification of 5G terminals provides a broad space for the development of various industries.

Global 5G commercial mobile phones are released one after another. Well-known manufacturers such as Huawei, Samsung, Xiaomi, OPPO and VIVO have successively released mass-produced 5G mobile phones. Samsung began selling Galaxy S10 5G mobile phones in April 2019, becoming the first mobile phone manufacturer in the world to announce the sale of 5G mobile phones. Huawei first launched Mate X, a commercial mobile phone based on 5G technology, at the Mobile World Congress in February 2019, and released Mate 20X 5G version in May 2019. In September 2019, Xiaomi launched two 5G mobile phones, Xiaomi 9 Pro 5G and Xiaomi MIX Alpha. It is estimated that there will be thousands of 5G mobile phones in 2021, which will greatly accelerate the penetration rate of 5G mobile phones.

Figure 21: Global 5G Mobile Phone Shipment Forecast

Figure 22: Global number of 5G terminals (November 2019)

Source: GSA, China Merchants Bank Research Institute

China’s 5G mobile phone market has great growth potential.

China is the world’s largest market for 5G smartphones. By the end of 2018, the number of mobile phone users in China was close to 1.2 billion, and the user penetration rate reached 82% of the total population, which was close to 85% in developed countries in Europe and America. In 2018, the global smartphone shipments were 1.456 billion, of which the total sales volume in China market was 398 million, accounting for 27%. Among the Top6 smartphone manufacturers in the world, Huawei, Xiaomi, OPPO and VIVO in China occupy four seats. In the second quarter of 2019, Huawei surpassed Apple to become the second largest smartphone manufacturer in the world. According to the GSMA forecast, by 2025, the global market share of 5G mobile phones will reach 15%, including 59% in South Korea, 50% in the United States, 48% in Japan, 29% in Europe and 28% in China. By 2025, the number of users of 5G mobile phones in China will exceed the sum of North America and Europe, reaching 460 million, making it the largest market for 5G smart phones.

The development speed of 5G mobile phones exceeded expectations. South Korea is the first country in the world to start large-scale commercialization of 5G. On April 3, 2019, Korean operators launched 5 G commercial services. At the beginning of May, the number of 5G users in South Korea reached 260,000. On June 10th, the 69th day of South Korea’s 5G commercialization, the number of 5G users reached 1 million, which was 11 days shorter than the time it took for 4G users to break through 1 million. At the beginning of August 2019, the number of 5G users in South Korea reached 2 million, faster than the same period of 4 G. The success of South Korea’s 5G business directly promoted the sales of Samsung’s 5G version of Galaxy Fold and Galaxy Note 10. According to the statistics of China’s Ministry of Industry and Information Technology, as of October 8, 2019, there were nearly 10 million subscribers to China’s 5G package, including 5.8 million from China Mobile, 1.99 million from China Unicom and 2 million from China Telecom. On November 1, 2019, China officially commercialized 5G networks. On November 20, 2019, the Ministry of Industry and Information Technology revealed that China’s 5G users signed 870,000 contracts. Xu Zhijun, the rotating chairman of Huawei, predicts that the number of 5G users in China will exceed 200 million in 2020.

Figure 25: Comparison of popularization speed of 4G/5G users in South Korea

Source: Zdnet, China Merchants Bank Research Institute

Figure 26: China Mobile’s 4G base station and user growth trend

Source: Wind, China Merchants Bank Research Institute

Investment rhythm of 5G mobile phone market

The scale of the 5G mobile phone market will exceed the investment scale of the 5G network. Looking back at the domestic 4G market, 4G licenses were issued in December 2013, and large-scale 4G network construction began in 2014. The growth of 4G users is in step with the construction of 4G networks, and the growth rate of 4G users is much higher than that of 4G base stations in the same period. In 2016, when the peak of 4G capital expenditure ended, the penetration rate of 4G users has reached 80%, and the replacement speed of 4G mobile phones is higher than the investment speed of 4G networks. Compared with the time rhythm of 5G network licensing and network construction, it can be predicted that the growth rate of 5G mobile phone market will also exceed the investment speed of 5G network. According to the forecast data of many institutions, in 2020, the market size of 5G mobile phones is expected to exceed 500 billion yuan. With the increasing proportion of sales of 5G mobile phones, the future 5G mobile phone market is expected to go to trillion scale, and there are great investment opportunities in the RF, camera, acousto-optic devices and other sub-sectors of the upstream supply chain of 5G mobile phones.

2020-2022 ushered in the peak of 5G replacement. From the history of 4G network construction and user growth, it can be predicted that 2020 will be the first year of 5G mobile phone explosion, and 2020-2022 will be the peak period of 5G replacement. By then, 5G mobile phones will drive the global smart phones to resume positive growth. In terms of the rhythm of the 5G terminal market, it is expected that the first half of 2020 will be in the market introduction period, and the second half of 2020 will enter the scale development period. Terminal manufacturers will launch low-and medium-priced products, and the scale of the 5G mobile phone market will continue to expand. It is estimated that by the end of 2020, the price of 5G mobile phone products will drop to 1500 yuan, and the market will be dominated by 5G mobile phones. In 2021, there will be a thousand yuan 5G mobile phone. Non-5G mobile phones and low-priced 5G mobile phones are expected to fully enter the ODM era, and the ODM market share will gradually expand.

3.2 5G IOT terminal market has great growth potential.

5G unified standards to promote the faster development of the Internet of Things

There are many standards of Internet of Things, which affect the development speed of the industry. The concept of Internet of Things began in 1998, and its vision is that everything in life can transmit information through network connection and realize the digitalization of the world. Due to the diversity of Internet of Things requirements, a number of Internet of Things technical standards have emerged. Power consumption, bandwidth, coverage distance and communication frequency have become the main factors in choosing Internet of Things technology. The existing technical standards of Internet of Things include Zigbee, WiFi, Bluetooth for short-distance communication technology and 2G, 4G, LoRa, SigFox, eMTC, NB-IoT for long-distance communication technology. Low-power wide area network (LPWAN) standard has become the designated mobile communication standard to meet the requirements of low power consumption, long distance and low bandwidth in Internet of Things applications, among which LoRa, SigFox and eMTC and NB-IoT with licensed spectrum have gradually emerged.

5G is expected to unify standards and promote the faster development of the Internet of Things. Unauthorized spectrum technology (LoRa, SigFox) can only be used in a small area due to the limitation of spectrum sharing. Authorized spectrum technologies (NB-IoT and eMTC) have already had the scale effect with the gradual deployment in the world. As of September 2019, at least 114 operators in 57 countries have deployed NB-IoT or eMTC, and 153 operators in 72 countries are actively investing in NB-IoT networks. In July 2019, 3GPP formally submitted the proposal of 5G candidate technical standards to ITU-R (International Telecommunication Union), and NB-IoT became the technical standard to meet the needs of 5G large-scale machine connection (mMTC) scenarios.

Figure 29: NB-IOT and eMTC network deployment

Source: GSA, China Merchants Bank Research Institute

Figure 30: Prediction of the number and scale of global Internet of Things terminals

Source: Ericsson and China Merchants Bank Research Institute.

High Growth Opportunity of Internet of Things Terminal Market

The global Internet of Things terminal market is expected to maintain rapid growth. IDC predicts that the global Internet of Things expenditure will reach $745 billion in 2019 and $1.1 trillion in 2023. Ericsson predicts that in 2025, the global Internet of Things terminal scale will reach 24.9 billion, among which short-range IoT devices (Wi-Fi, Bluetooth and Zigbee) will reach 19.5 billion, with a compound annual growth rate of 13%; Wide-area IoT devices (2G, 3G, 4G, 5G, NB-IoT, eMTC, Sigfox and LoRa) reached 5.4 billion, with a compound annual growth rate of 24%. In 2025, among the wide-area IoT devices, NB-IoT and eMTC devices are the 5G mainstream IOT terminals, accounting for 52%; 4G and 5G large bandwidth IoT terminals accounted for 28%. In the long run, the market size of IOT terminals far exceeds that of smart phones.

Figure 31: Prediction of the number and scale of terminals in the global wide-area Internet of Things

Source: Ericsson and China Merchants Bank Research Institute.

Figure 32: Distribution of NB-IoT New Products in China in 2019Q1

Source: Institute of ICT, China Merchants Bank Research Institute.

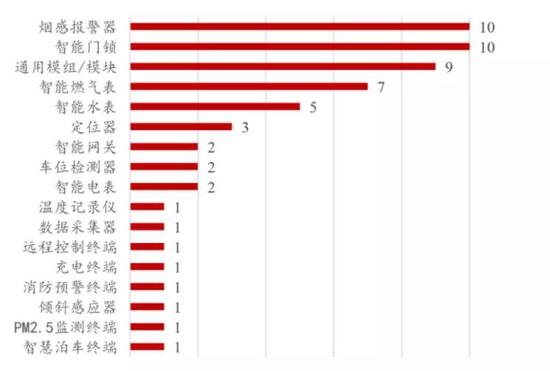

China’s Internet of Things terminal market is growing rapidly. By the end of 2018, the Internet of Things connection terminals of China’s three major operators had exceeded 760 million, of which China Mobile’s Internet of Things connection scale reached 551 million. The existing IOT terminals still mainly use 2G/3G/4G networks, and the proportion of NB-IoT/eMTC terminals is still small. Under the impetus of 3GPP, NB-IoT is included in the 5G standard, which ensures the smooth upgrade of operators NB-IoT to 5G network and is conducive to the rapid promotion of NB-IoT terminals. China’s NB-IoT terminals have been widely deployed, and have developed rapidly in the application fields of smart home, smart city, intelligent production and intelligent logistics. According to the statistics of China ICT Institute, in the first quarter of 2019, 58 new NB-IoT terminal products were listed. Since 2018, the number of NB-IoT terminals has accumulated to 180. From the product form, it covers smart meters, smart door locks, flammable gas alarms, locators, and general modules/modules that can be widely used in the field of Internet of Things.

In the short term, the smart home terminal market is the largest. According to Strategy Analytics, the total expenditure of global smart home market (equipment, system and service consumption) will be close to $96 billion in 2018, with a compound annual growth rate of 10% in the next five years (2018-2023), and the global smart home market will reach $155 billion by 2023. The North American market is dominated by Amazon, Google and Samsung; There are British companies Centrica Connected Homes’Hive and Deutsche Telekom’s Magenta Home, German eQ-3 and Dutch Enco’Toon; in the European market. In the Asia-Pacific region, there are Xiaomi in China, LG in South Korea, iTSCOM and Panasonic in Japan. The smart home market is still highly fragmented and has great growth opportunities.

Figure 33: Global Smart Home Market Scale

Source: Strategy Analytics and China Merchants Bank Research Institute.

Figure 34: China Internet of Things Market Growth Forecast (2017-2022)

Source: IDC, China Merchants Bank Research Institute

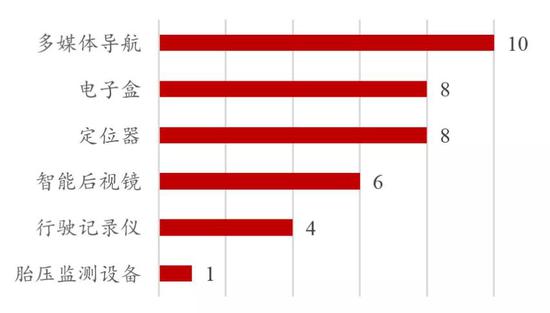

In the medium term, the car networking terminal market has the highest growth rate. Gartner predicts that by 2023, the automotive industry will become the largest market for 5G IoT solutions, accounting for 53% of 5G IoT terminals. IDC predicts that among the mainstream application scenarios in China in the next five years, the car networking scenario will grow fastest. From the overall situation of the domestic vehicle terminal market, in Q1 of 2019, 37 new products of vehicle terminals were listed, including 6 2G terminals, 1 3G terminal, 29 4G terminals and 1 NB-IoT terminal. From the application field, the current vehicle-mounted mobile terminal products include not only general equipment for cars, buses and trucks, but also special terminals for certain models, such as Beidou compatible terminals for logistics vehicles. From the product form, it includes not only intelligent rearview mirrors and vehicle-mounted robots with high integration, but also driving recorders, vehicle navigation and ETC intelligent terminals focusing on specific functions. With the advancement of the Internet of Vehicles, consumers have higher and higher requirements for the intelligence of vehicle-mounted mobile terminals, and more and more vehicle-mounted mobile terminals are equipped with intelligent operating systems such as Android. In Q1, 2019, there were 14 new smart car mobile terminals equipped with operating systems, accounting for 37.8% of the newly listed models in the same period.

Figure 35: Distribution of new products on the market of domestic vehicle terminals in Q1, 2019.

Source: Institute of ICT, China Merchants Bank Research Institute.

Figure 36: Industrial Internet of Things Application Scenario

Source: PTC, China Merchants Bank Research Institute

In the long run, the Industrial Internet of Things (IIoT) will become the largest market for the 5G Internet of Things. GSMA mobile think tank predicts that by 2025, the number of smart manufacturing connections in the Asia-Pacific region will reach more than 530 million. According to the survey data of industrial Internet of Things software platform PTC on its customers, the leading industry in deploying industrial Internet of Things solutions is industry (25%), followed by electronics and high technology (23%) and automobile industry (13%). Specific application scenarios include manufacturing/operation, service, product design and IT. The most important application scenario is the formation of manufacturing operation information and operational asset monitoring by using the Internet of Things. These intelligent industrial connection functions can help product manufacturers improve their output and production quality, and reduce manufacturing costs.

4.5G industry cloud has a long-term development prospect in the vertical field.

From the perspective of application scenarios, 5G promotes the integration of cloud network services, and gradually evolves from a cloud platform providing virtualized basic resources to an industry cloud applied in typical industries, which not only drives the rapid growth of data centers, but also deeply integrates in real economic fields such as education, security, energy and industry, creating new kinetic energy for economic development.

Figure 37: Global Cloud Computing Market Size and Growth Forecast

Source: Gartner, China Merchants Bank Research Institute.

Figure 38: Global IaaS Public Cloud Market Share

Source: Gartner, China Merchants Bank Research Institute.

4.1 Cloud network convergence promotes the rapid development of cloud computing industry

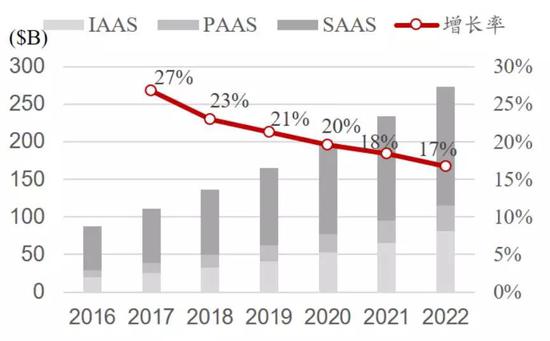

The global cloud computing market continues to grow steadily. In 2018, the global public cloud market reached US$ 136.3 billion, with a growth rate of 23%. It is estimated that in 2022, the global public cloud market will reach US$ 270 billion, in which the compound annual growth rate of IaaS is over 26%, that of PaaS is over 20%, and that of SaaS is over 14%. The global market concentration trend is obvious. From the perspective of IaaS revenue in 2018, the top three occupy 70% of the global market share. Among them, Amazon AWS still occupies the first place, with a market share of 51.8% and a growth rate of 26.8%; Microsoft Azure followed closely, with a market share of 15.5% and a growth rate of 61%; Alibaba Cloud ranks third with a market share of 7.7%, with a growth rate of 93%.

The growth rate of China’s cloud computing market is higher than the global level, and the public cloud market is growing faster than the private cloud market. In 2018, the overall market size of cloud computing in China reached 96.28 billion yuan, with a growth rate of 39.2% higher than the global level. Among them, the size of the public cloud market reached 43.7 billion yuan, up 65% year-on-year; The scale of the private cloud market reached 52.5 billion yuan, a year-on-year increase of 23%. From the public cloud IaaS, Alibaba Cloud, Tianyiyun and Tencent Cloud occupy the top three; From the public cloud PaaS, Alibaba Cloud, Tencent Cloud and Baidu Cloud occupy the top three; From the perspective of public cloud SaaS, UFIDA, Kingdee and Changjietong occupy the top three. According to the prediction of World Information, an ICT research consultancy, in 2018, the cloud access rate of enterprises in China will be around 30%, while that of enterprises in the United States will be around 80%. There is still a lot of room for growth in the cloud computing market in China in the future.

Figure 39: Market Size and Forecast of Public Cloud in China

Source: Institute of ICT, China Merchants Bank Research Institute.

Figure 40: China Private Cloud Market Scale and Forecast

The rapid growth of cloud computing promotes the continuous growth of data centers. Due to the rapid development of cloud computing, search, social networking, e-commerce and payment services, the global demand for data centers is growing day by day, and the ultra-large-scale data centers continue to grow rapidly. According to the Cisco Global Cloud Index CGCI, from the end of 2016 to 2021, the number of very large-scale data centers in the world will increase from 338 to 628; The global annual data center traffic will increase from 6.8ZB to 20.6ZB, with a compound annual growth rate of 25%. The continuous growth of Internet traffic has promoted the continuous expansion of data centers. In 2018, the market size of IDC in China reached 122.8 billion yuan, and it will reach 275.9 billion yuan in 2021, maintaining a growth rate of about 30%.

4G services promote the high growth of data center traffic. There is a positive correlation between the growth of network traffic of operators and the growth of data traffic in data centers. The traffic of 4G, private line and broadband services in the operator’s network comes from the content server in the data center. The outbreak of Internet services and the acceleration of operators’ pipelines can effectively increase the traffic demand of data centers. As of October 2019, the scale of 4G users of three operators in China reached 1.269 billion, and the average mobile Internet access traffic (DOU) reached 8.54GB in that month, with an increase rate of 85.6% year-on-year. The demand for data centers increased rapidly with the synchronization of 4G services.

Figure 41: China IDC market size forecast

Source: China IDC Circle, China Merchants Bank Research Institute.

Figure 42: 4G services drive data center traffic growth

Source: China Merchants Bank Research Institute

4.2 5G industry cloud has long-term investment opportunities.

5G promotes the rapid development of data centers.

Figure 43: DoU trend of 4G/5G users in South Korea

Source: Zdnet, China Merchants Bank Research Institute

Figure 44: DoU trend forecast of China Mobile’s 4G/5G users.

Source: China Mobile and China Merchants Bank Research Institute.

5G effectively enhances DoU, which will drive the data center to maintain rapid growth in the next three years. The growth rate of monthly Internet traffic (DoU) of operators directly reflects the growth rate of data center traffic. According to the statistics of Korea Ministry of Science and Information, in Q2 of 2019, South Korea’s 5G DOU was 24GB, while 4GDoU was 9.5GB, and 5G DoU was three times that of 4GDou. According to the forecast of China Mobile, the 5G DoU will be 19.6GB in 2019 and 37.8G in 2022, with a compound annual growth rate of 25%. With the gradual promotion of 5G, 5G DoU is three times that of 4G Dou, which will drive the data center to maintain rapid development in the next three years.

5G solves network bottleneck, and cloud games meet development opportunities.

The characteristics of large bandwidth and low latency of 5G solve the bottleneck of the development of cloud games. Cloud games are based on cloud computing technology. The data processing of the games is not run locally, and there is no need to download the games. All the games are run in the cloud, and the server in the cloud will transmit the game images to the user terminal through the network after data compression. Cloud games greatly reduce the configuration requirements for user terminals. User terminals do not need to use any high-end hardware configuration, but only need to meet the simple video streaming media processing ability, and are responsible for sending operation instructions and accepting returned video information. The advantages of low threshold, multi-device synchronization and immediacy of cloud games also bring corresponding demands. Cloud games need more network bandwidth and lower network delay than traditional games, and network bottleneck has become one of the main factors for poor user experience of cloud games. With the arrival of 5G, the large bandwidth and low latency of 5G can bring users a high-quality cloud game service experience.

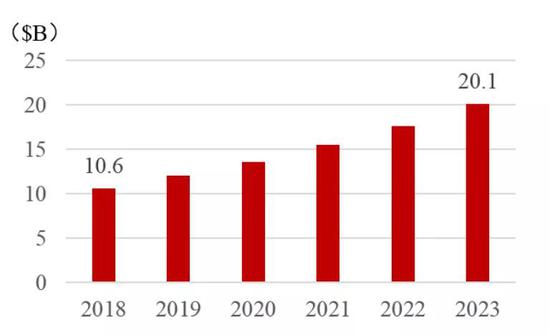

The cloud game market has great potential for long-term development. IHS Markit predicts that by the end of 2019, the market size of cloud games will exceed 500 million dollars for the first time, and by the end of 2023, the market size of cloud games will reach 2.5 billion dollars. Market research company Niko predicts that China will become the world’s largest cloud game market in 2023, when the revenue of China’s cloud game market will exceed 1.1 billion US dollars.

Industry giants have entered one after another, and cloud games and social interaction are deeply integrated. In November 2019, Google officially launched the cloud game platform Stadia, which supports smart terminals such as laptops, tablets, mobile phones and TV boxes, and the screen can be seamlessly switched. Google has brought many new ways to play, which can share the video and screenshots of the game to the video website with one click, and the content of the video and trailer of the game will provide the entrance to the game, so as to realize instant play. Players can share their own game progress through the connection, and other players can join in the cooperative game at any time; The anchor can invite the audience to participate in the game and interact at any time when the game is broadcast live. Tencent cloud game platform WeGame was launched in August 2019, and Netease cloud game platform has also been launched, includingOther small manufacturers, such as Red Finger Cloud Mobile Phone and Hai Mayun, have also actively launched cloud game services.

Cloud game ecology is diversified, and new business models are constantly emerging. Domestic cloud game business models mainly include virtual mobile phone rental, game joint operation and playable game advertisements. The virtual mobile phone rental mode is the main mode in the To C market. Users can hang up in the cloud to brush their experience and resources by purchasing virtual mobile phones with different configurations. Joint operation mode with game manufacturers, similar to Apple App Store, cloud game platform can be jointly operated with multiple game manufacturers to help game manufacturers bring new user traffic. The playable game advertising mode breaks through the traditional static and video game advertising mode, and the advertising window is the game entrance, which is helpful to directly improve the user’s advertising conversion rate.

Cloud games directly drive the growth of cloud computing resources. Cloud games bring customers a perfect experience, and put a lot of game data processing and picture rendering in the cloud. Cloud games directly drive the growth of demand for cloud computing and data center resources, and the growth of demand for servers, storage, network equipment and chips that meet high-quality image processing. The combination of cloud games with smart hardware such as mobile phones, PADs, PCs, AR/VR, TVs, etc. may become the killer application of To C services in the 5G era.

5G promotes new opportunities in new areas of security

The three characteristics of 5G bring more security application scenarios. In the next few years, the demand for security technology products at home and abroad will maintain a steady growth trend, with strong security demand in many industries such as cities, transportation, education, medicine, environment and finance. In 2018, the market size of video surveillance equipment in China was US$ 10.63 billion. IDC predicts that by 2023, the market size of video surveillance equipment in China will reach $20.13 billion, with a compound annual growth rate of 13.6%. With the arrival of 5G, the three characteristics of large bandwidth, large connection and low delay bring more cloud security application scenarios, realizing new requirements such as high-definition monitoring, AR glasses/helmet inspection, drone inspection, material monitoring, fire alarm monitoring and emergency command.

Cloud network cooperates to meet the diversified needs of security services. Cloud security platform can not only reduce the implementation cost of security projects and improve the deployment efficiency of security business, but also realize the linkage between security business and other social public departments and improve the efficiency of social operation. The combination of cloud AI deep learning based on GPU and FPGA and the AI computing power of edge cameras greatly improves the ability to analyze and identify people, cars and things. After computer vision processing and deep learning, the ability of target classification and attribute recognition can be easily realized. In the future, security terminal equipment can realize full video feature structure through AI chip, and then transmit feature information to edge cloud and central cloud through 5G network, and the cloud can maximize efficiency through intelligent analysis. The diversification of cloud security application scenarios has led to new development opportunities for cloud computing in the security field.

Figure 47: China Video Surveillance Market Scale Forecast

Source: IDC, China Merchants Bank Research Institute

Figure 48: 5G Intelligent Security Solution

Source: China Merchants Bank Research Institute

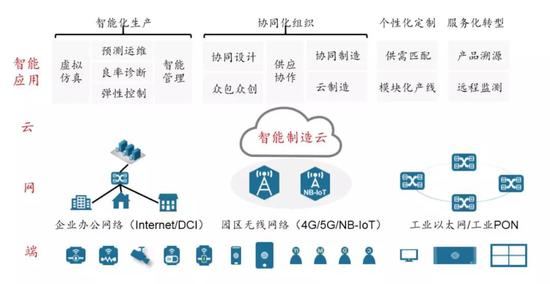

5G accelerates the cloudization of industrial manufacturing and realizes digital transformation

5G Industrial Internet unleashes unlimited potential for manufacturing. Industrial Internet has promoted the formation of a brand-new industrial manufacturing and service system through the comprehensive interconnection of people, machines and things, and is an important cornerstone of the fourth industrial revolution. Industrial Internet provides a key support for the digitalization, networking and intelligent upgrading of manufacturing industry, which is conducive to the birth of new models and new formats, and promotes the transformation and upgrading of traditional industries and the cultivation and growth of new kinetic energy. At present, China’s manufacturing industry is still at a low level, limited by the low level of automation, insufficient level of informatization, unresolved problems of networking and real-time data transmission, and the industrial Internet is still in its infancy. 5G’s ultra-large bandwidth, ultra-large connection and ultra-low latency make it possible for the industrial Internet to make great strides.

Cloudization of industrial manufacturing brings long-term investment opportunities. According to the analysis of ICT Institute, at this stage, China’s manufacturing enterprises mainly focus on the cloudization of simulation design, business system and industrial Internet of Things. In the simulation design, such as automobile, heavy industry, complex electrical appliance manufacturing enterprises, through high-performance computing on the cloud, simulate the real environment, and carry out multi-scene design analysis. The business system provides flexible resource allocation for business systems such as manufacturing, finance, sales, inventory, procurement and service through the cloud platform, which improves efficiency and saves a lot of costs. Industrial Internet of Things collects, analyzes and manages data through tens of thousands of terminals in the cloud. Industrial intelligent manufacturing goes to the cloud, which promotes China’s development from a manufacturing power to a manufacturing power, and also brings broad business opportunities for cloud computing.

Figure 49: Cloudization of industrial manufacturing